DeFi's Next Act III: Why Identity Is the Missing Layer of DeFi

The first wave of DeFi proved something important: blockchains can move value without intermediaries.

The second wave showed that liquidity fragments easily. AMMs multiplied, pools splintered, and capital scattered across chains and rollups. The most successful platforms—like Hyperliquid—won by unifying liquidity around a shared order book.

But a deeper problem remains unresolved:

Credit requires identity.

Not identity in the Web2 sense of exposing personal data.

But identity in the financial sense: eligibility, reputation, compliance, accountability.

If DeFi wants to graduate from speculation to real-world capital markets, identity cannot remain an afterthought. It must become part of the architecture.

Institutional Capital Is Coming, But It Plays by Different Rules

For years, DeFi could ignore compliance because most capital was crypto-native.

That era is ending.

- Stablecoin issuers are regulated.

- Funds are regulated.

- Institutions are regulated.

- Even treasuries and corporations experimenting with DeFi are regulated.

If public blockchains want to serve real-world finance, we have to understand something simple:

Institutional capital does not move without eligibility rules.

And those rules aren't optional.

So let's ask the uncomfortable questions:

- How does a U.S. institution lend their Bitcoin only to U.S. borrowers?

- How does an accredited-only fund restrict participation?

- How does a regulated stablecoin issuer prevent sanctioned entities from borrowing?

Without identity, we cannot attract institutional capital.

But if we bolt identity in the wrong way, we fragment liquidity and destroy the openness that makes DeFi powerful.

So the solution cannot be “no KYC.”

And it cannot be “hardcode KYC into every smart contract.”

It has to be architectural.

A Shared Order Book for Credit

On Cardano, a peer-to-peer lending model can be surprisingly simple.

Each loan request can exist as a UTxO: an unspent output on the blockchain that holds funds and rules.

A borrower could:

- Lock collateral in a UTxO

- Attach loan terms in its data

- Tag it with a small marker token

These marker tokens are sometimes called beacon tokens. They simply act as labels, allowing indexers to easily discover all open loan requests.

They can also reference additional requirements attached to the loan — for example proof that a legal agreement exists between the parties, or that certain contractual terms have been accepted off-chain.

In effect, the blockchain becomes a public message board for credit.

Borrowers post requests → lenders submit competing offers → anyone can scan the chain and see available loans.

This creates a shared order book for lending, without relying on centralized databases.

But on its own, this structure still lacks one thing: eligibility.

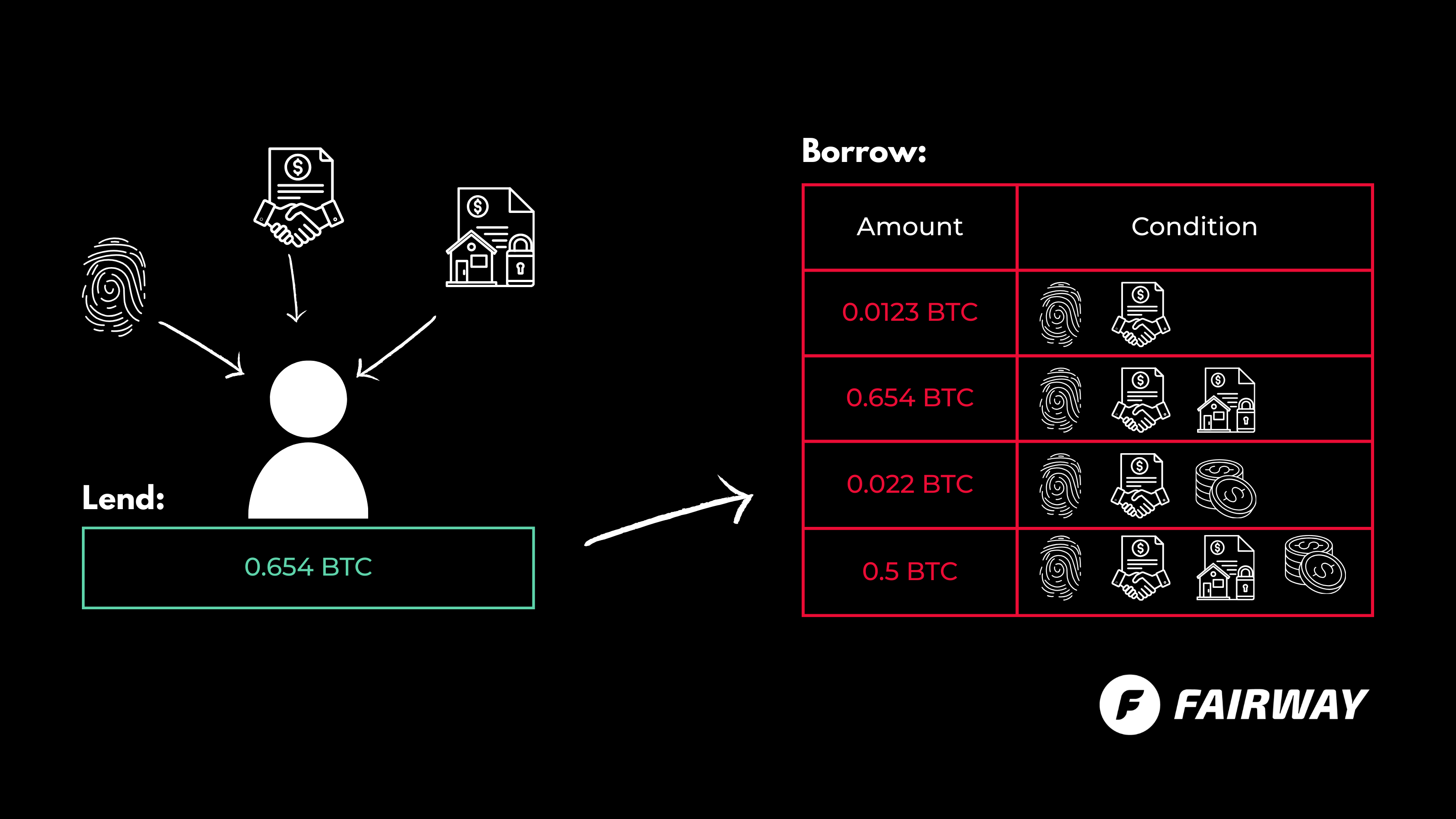

Where Identity Enters the Picture

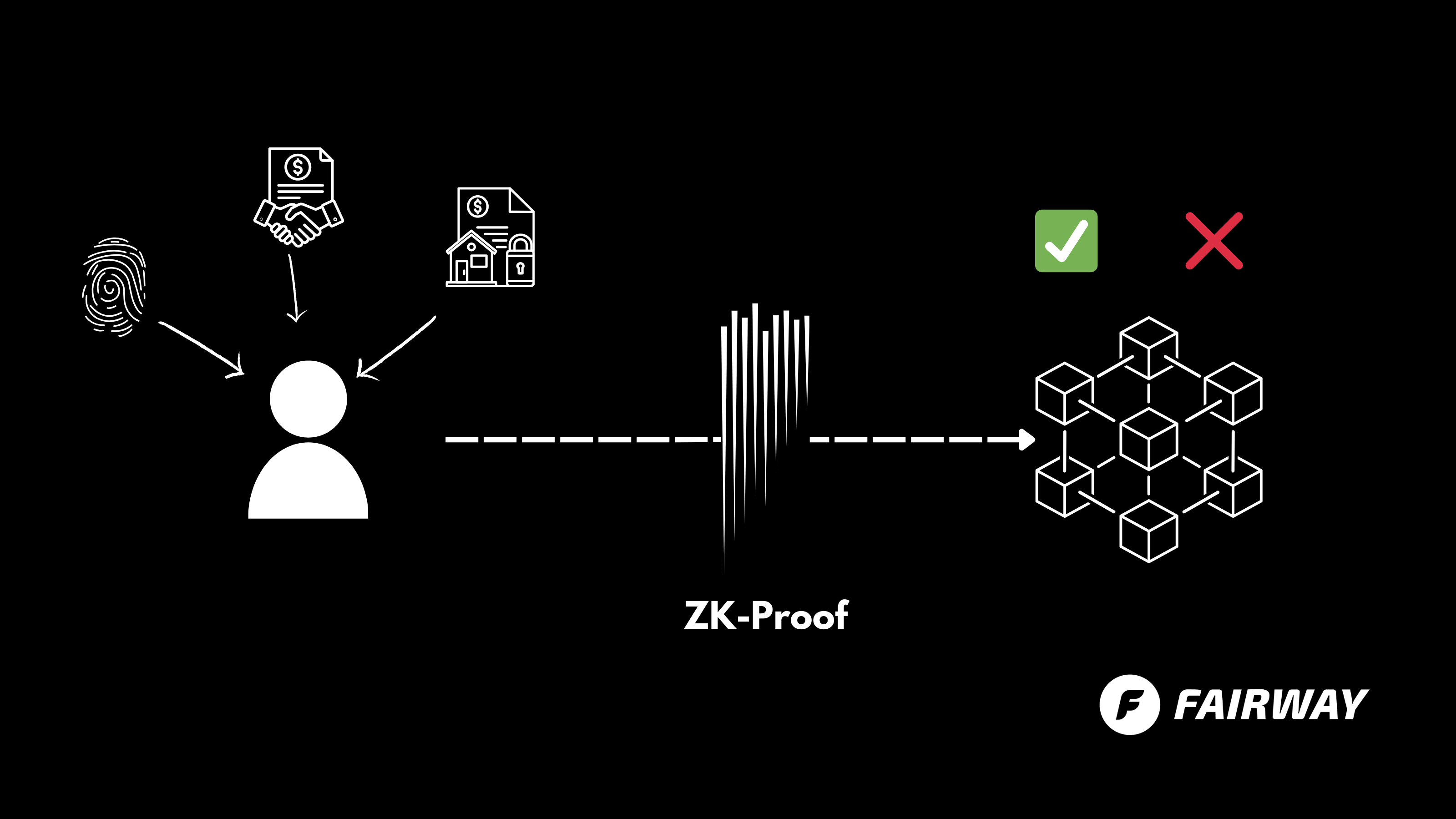

Now imagine a borrower posts a loan request.

Alongside the loan terms, they attach cryptographic proofs generated from verified credentials.

These credentials can represent many different attributes relevant to lending, for example:

- KYC verification

- Jurisdiction (e.g. U.S. resident)

- Accreditation status

- Credit reputation or repayment history

- Proof that a legal agreement has been signed

- Compliance checks such as sanctions screening

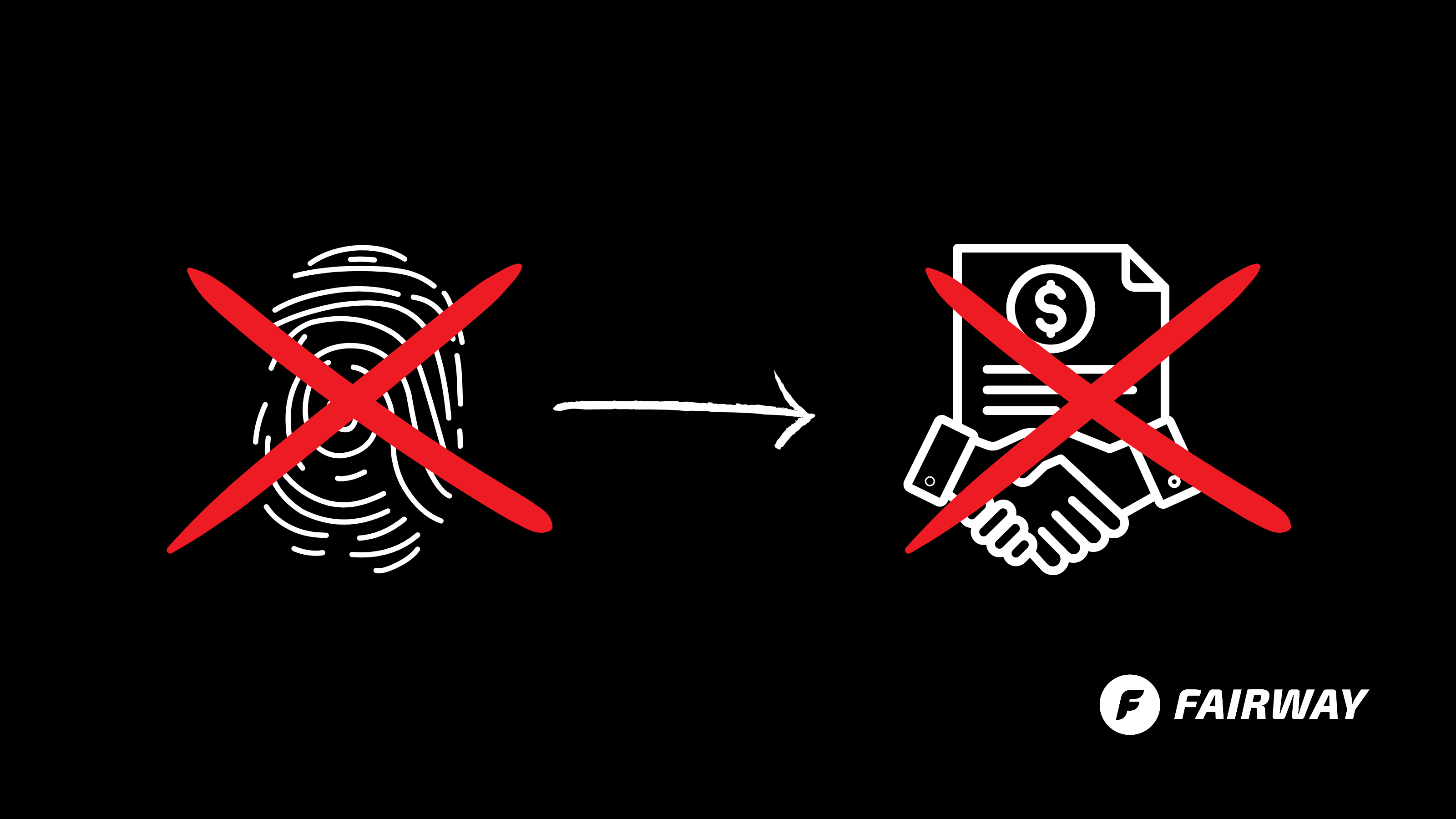

Importantly, these proofs do not reveal personal data.

They simply prove that a required condition is true.

For example, a proof might confirm:

- “This borrower is KYC verified.”

- “This borrower meets accredited investor requirements.”

- “A legally binding agreement exists between the parties.”

The underlying credentials can live privately — for example in Midnight, Cardano's privacy partner chain, which supports shielded accounts and confidential smart contracts.

Midnight handles sensitive identity state. Cardano handles public settlement.

Only the proof, not the personal data, is attached to the loan request.

Now the shared order book doesn't just show price and duration.

- It shows who is eligible to participate.

- Identity becomes part of liquidity discovery.

What benefits does Cardano's architecture provide here?

Cardano's extended UTxO model has a useful property here: each loan request is an independent object.

Instead of storing identity rules in a single global contract, each request carries its own verification proof.

This avoids maintaining large global registries and allows many transactions to be processed in parallel.

In practice, this makes it easier to represent individual credit agreements directly on-chain, while keeping identity verification flexible.

Compliance Without Closing the Network

One subtle design choice makes this model workable.

The protocol itself stays open, because compliance happens at the interface layer.

Anyone can technically post a loan request on-chain, but regulated wallets and indexers will only display requests that include valid proofs from recognized credential issuers.

This approach keeps the base network permissionless while allowing institutions to interact safely.

Identity as Infrastructure

In this architecture, identity isn't an add-on feature. It becomes infrastructure.

Instead of exposing personal data, identity providers can issue verifiable credentials that generate proofs used inside financial transactions.

These credentials can represent:

- KYC or KYB verification

- accreditation status

- jurisdictional eligibility

- compliance requirements

The blockchain only verifies the proofs. The identity data remains private.

This allows regulated capital to interact with open financial infrastructure — without sacrificing privacy or decentralization.

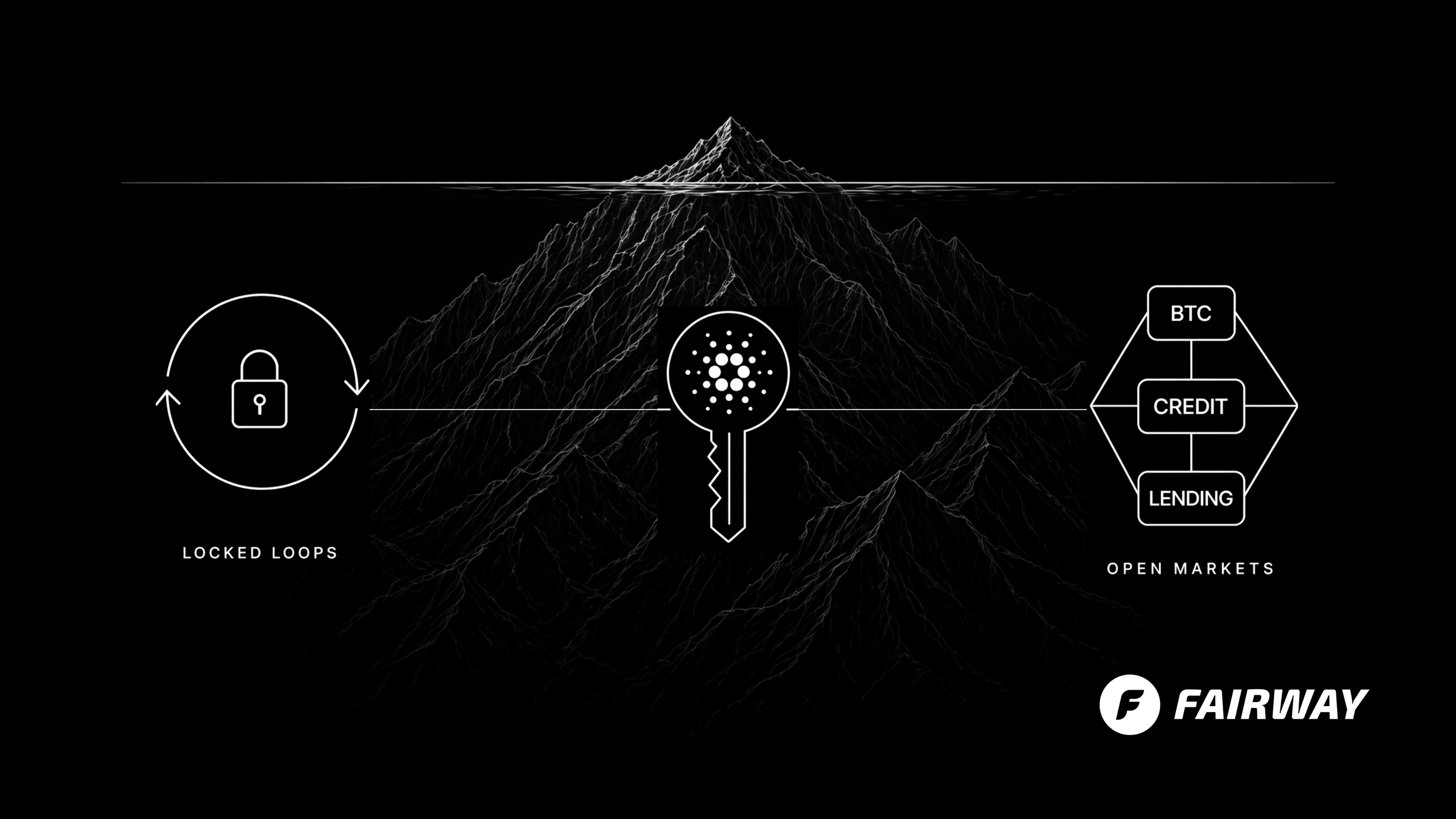

A New Phase for DeFi

For years, DeFi focused primarily on trading and leverage, but the larger opportunity has always been credit. Real financial markets are built on lending relationships, reputation, and enforceable rules. If shared order books solved liquidity for trading, the next step may be solving identity for credit.

Cardano's architecture, with deterministic execution and flexible identity proofs, offers one possible path toward that future.

The next phase of DeFi may not look like yield farming — it may look much closer to a global credit market.

And in that world, identity isn't optional.

It's the key that lets real capital participate.

Henrik Metsämäki

Expert in blockchain compliance and regulatory frameworks. Passionate about bridging traditional finance with decentralized technologies.