DeFi’s Next Act V: Cardano May Be Quietly Building Crypto’s Next Trillion-Dollar Product — And No One Even Notices

For more than a decade, crypto has claimed it would rebuild finance.

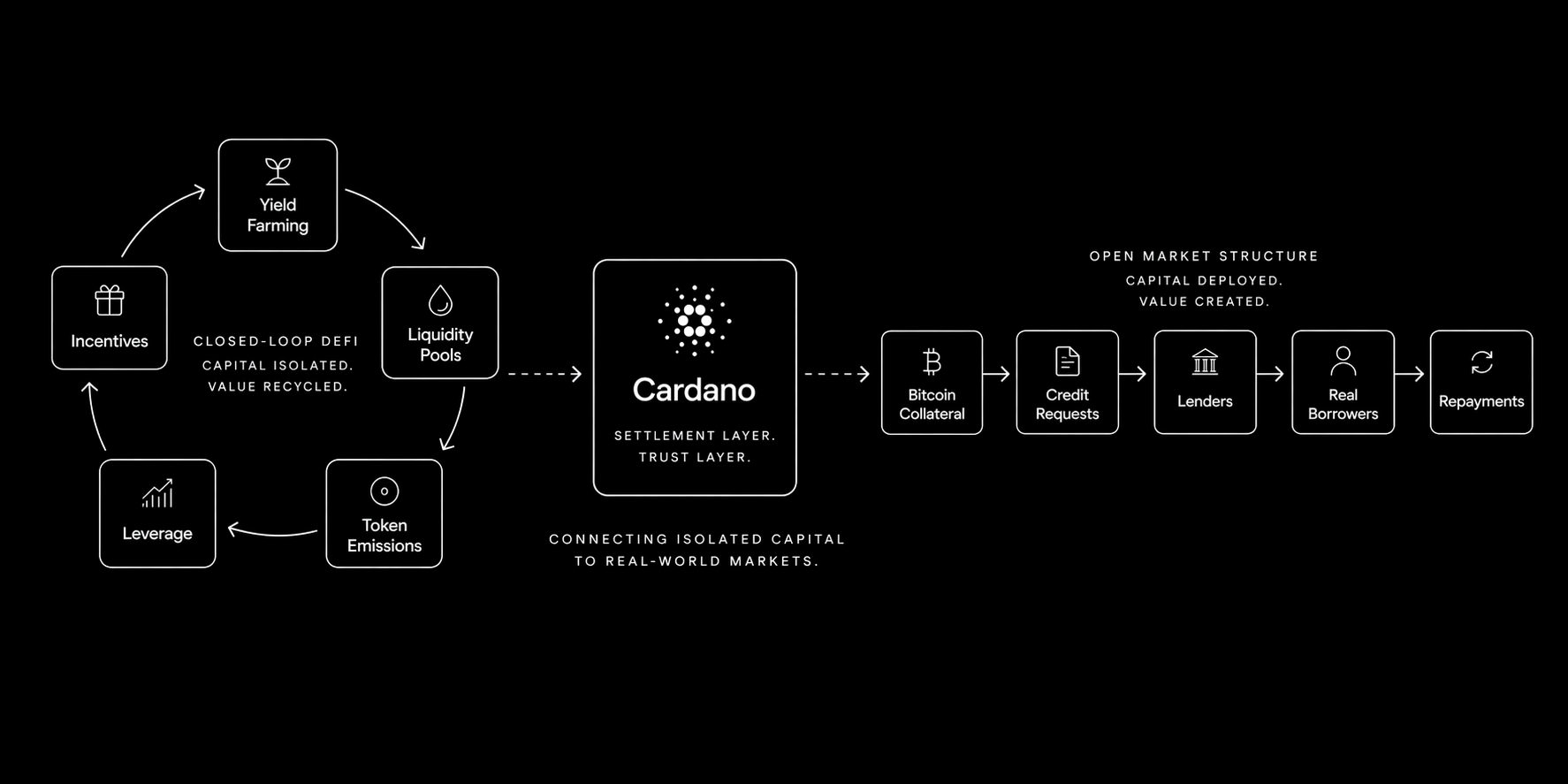

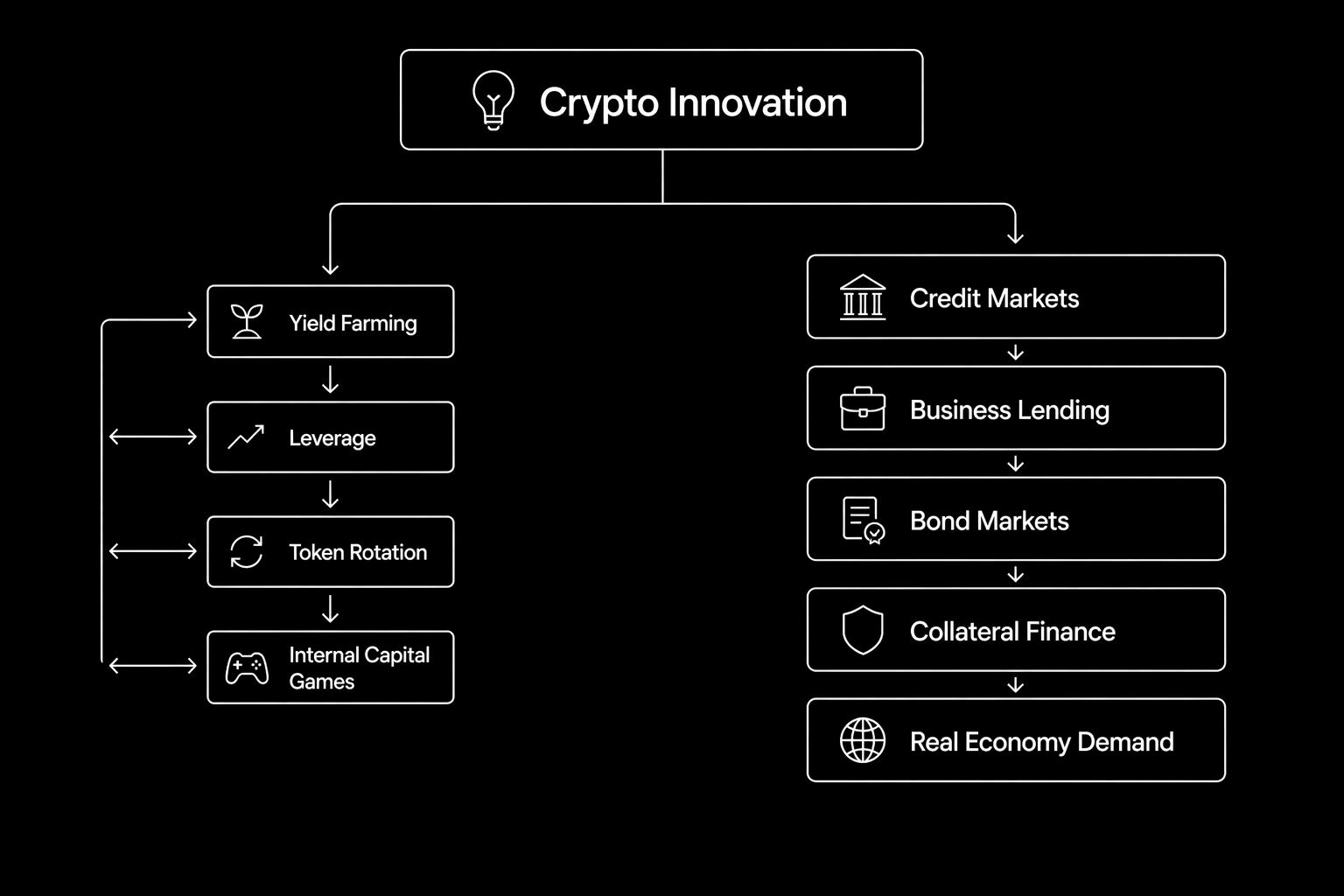

In one sense, it did. The industry created entirely new market structures: automated market makers, liquidity pools, yield farming, perpetual leverage, synthetic incentives, staking economies, token emissions, points programs, and endless variations of capital rotating inside crypto-native systems.

Some of these ideas were genuinely innovative. Many were profitable. Several changed how markets can be designed online.

But there was always a deeper question in the background:

Were these products solving large financial problems—or mostly optimizing activity within crypto itself?

That distinction matters now more than ever.

Because finance does not reward novelty on its own. It rewards usefulness at scale.

And if we are being honest, one of crypto’s clearest product-market-fit successes has not been a novel DeFi primitive at all. It has been stablecoins.

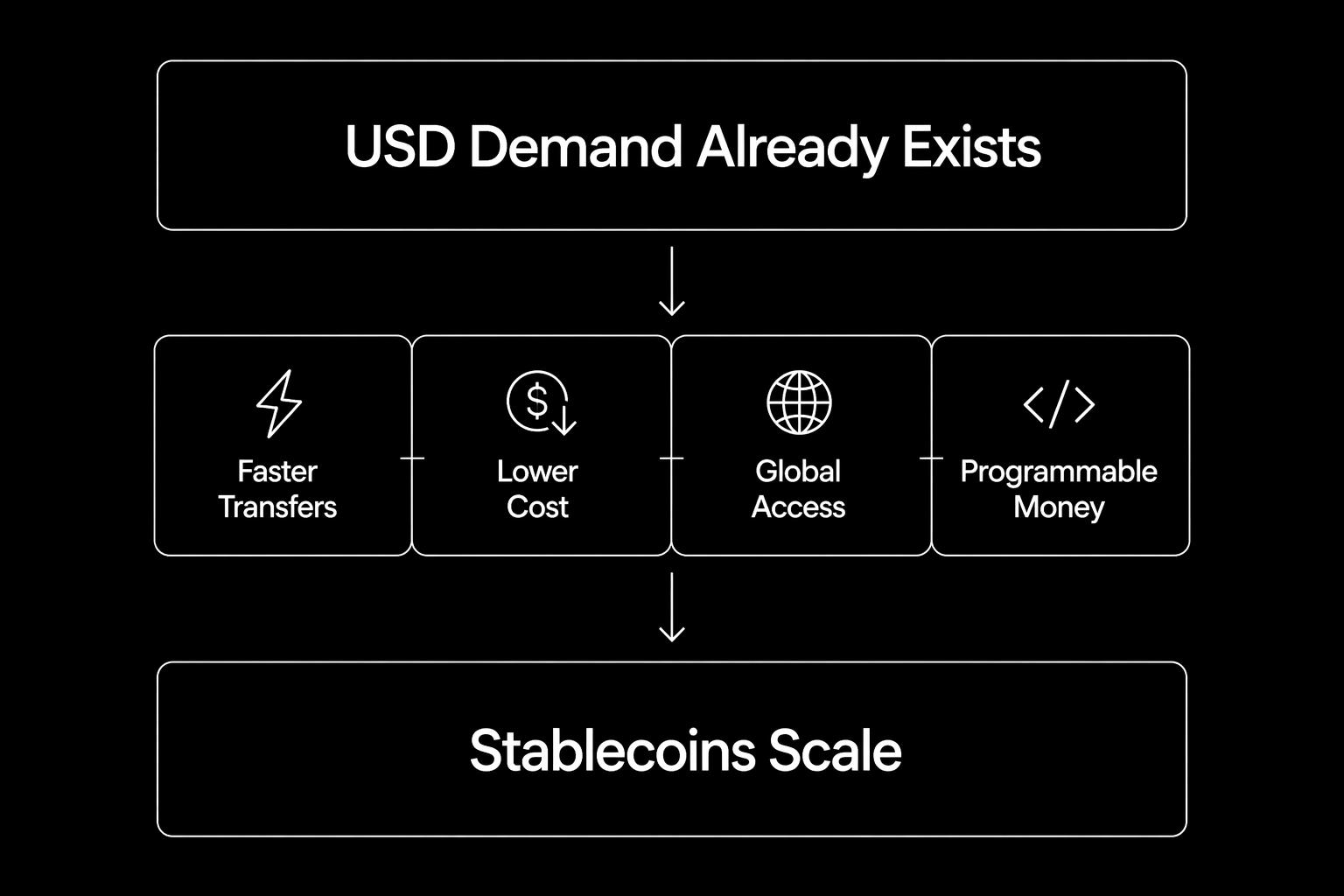

Stablecoins Succeeded for an Uncomfortable Reason

Stablecoins worked because the underlying demand already existed.

The U.S. dollar was already the world’s preferred settlement asset, reserve asset, and unit of account across large parts of global trade. Crypto did not create that demand.

“Stablecoins did not win because users wanted “crypto.” They won because users wanted dollars with better rails.”

It simply made dollars easier to move, easier to access, faster to settle, and more programmable.

That is a very different kind of success story than much of DeFi.

Stablecoins did not win because users wanted “crypto.” They won because users wanted dollars with better rails.

There is an important lesson in that.

Crypto’s biggest commercial opportunity may not be inventing endless new financial abstractions. It may be improving markets people already need.

DeFi’s Main Constraint Wasn’t UX

The industry often explains DeFi’s slower mainstream adoption as a usability problem.

And yes, wallet setup, key management, fragmented interfaces, bridging flows, and poor onboarding have all held users back.

But rough UX alone does not stop valuable products.

Bloomberg terminals are expensive and clunky. SWIFT is nobody’s favorite interface. Early online banking was awkward. Businesses still adopted them because the utility justified the friction.

“rough UX alone does not stop valuable products.”

The bigger issue for much of DeFi was simpler: many products were not tied to urgent, real-world demand.

They were efficient ways to deploy crypto capital against other crypto capital. That can create markets, but it does not automatically create broad product-market fit.

As a result, enormous talent went into optimizing speculation while much larger categories remained relatively untouched:

- credit markets

- private debt

- trade finance

- collateralized lending

- cross-border capital formation

- securitized assets

Those are not side markets. They are core markets.

“Real Finance Runs on Credit”

Traditional finance is not primarily built on token velocity, yield loops, or trading volume.

It runs on credit relationships.

Mortgages, business lending, municipal bonds, corporate debt, repo markets, equipment finance, receivables financing, project finance—these are the mechanisms through which capital gets allocated in the real economy.

They are also areas where blockchains should have something meaningful to contribute:

- faster settlement

- auditable collateral states

- programmable agreements

- reduced intermediation layers

- global access to capital pools

- better transparency across counterparties

Yet crypto often focused on what was easiest to launch under existing blockchain architectures, not necessarily what was most valuable to modernize.

That may now be changing.

Technology Shapes the Products People Build

A recurring pattern in technology is that builders create products their tools naturally support.

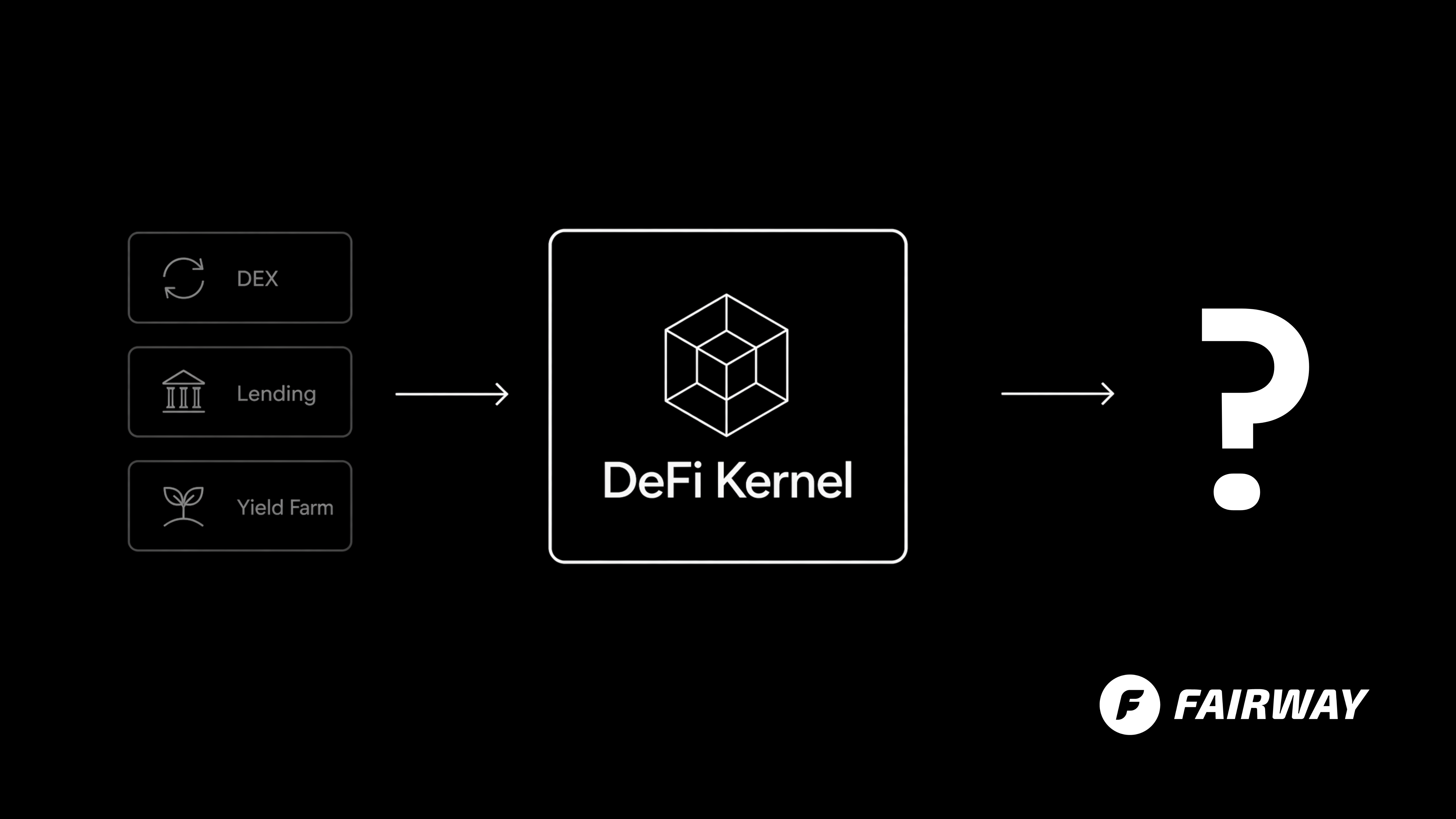

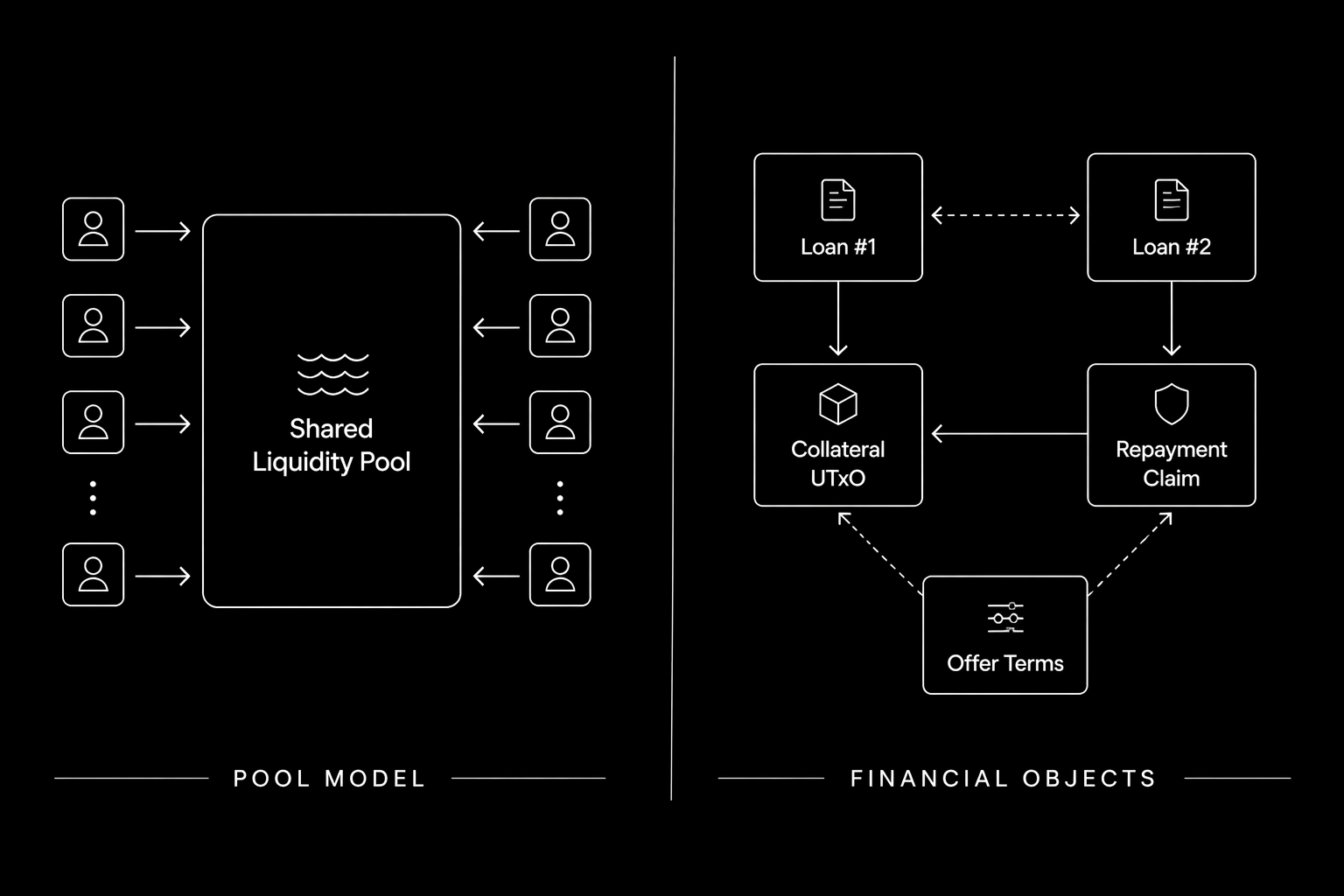

Much of DeFi grew on account-based systems that were well suited to pooled balances, shared liquidity, and highly composable application logic. Unsurprisingly, the dominant products became AMMs, lending pools, and strategies built around reusable on-chain liquidity.

Those systems were historically important. They proved that open financial infrastructure could attract real usage.

But they may not be the best structure for every financial market.

Many credit markets do not operate as pooled systems. They rely on discrete agreements with different terms, different risk profiles, different collateral, and different counterparties. A business loan is not the same as a mortgage. A secured BTC loan is not the same as unsecured working capital.

Real credit is heterogeneous.

That suggests a different market design: less like one shared pool, more like a marketplace of distinct financial contracts.

Why Cardano May Matter More Than People Think

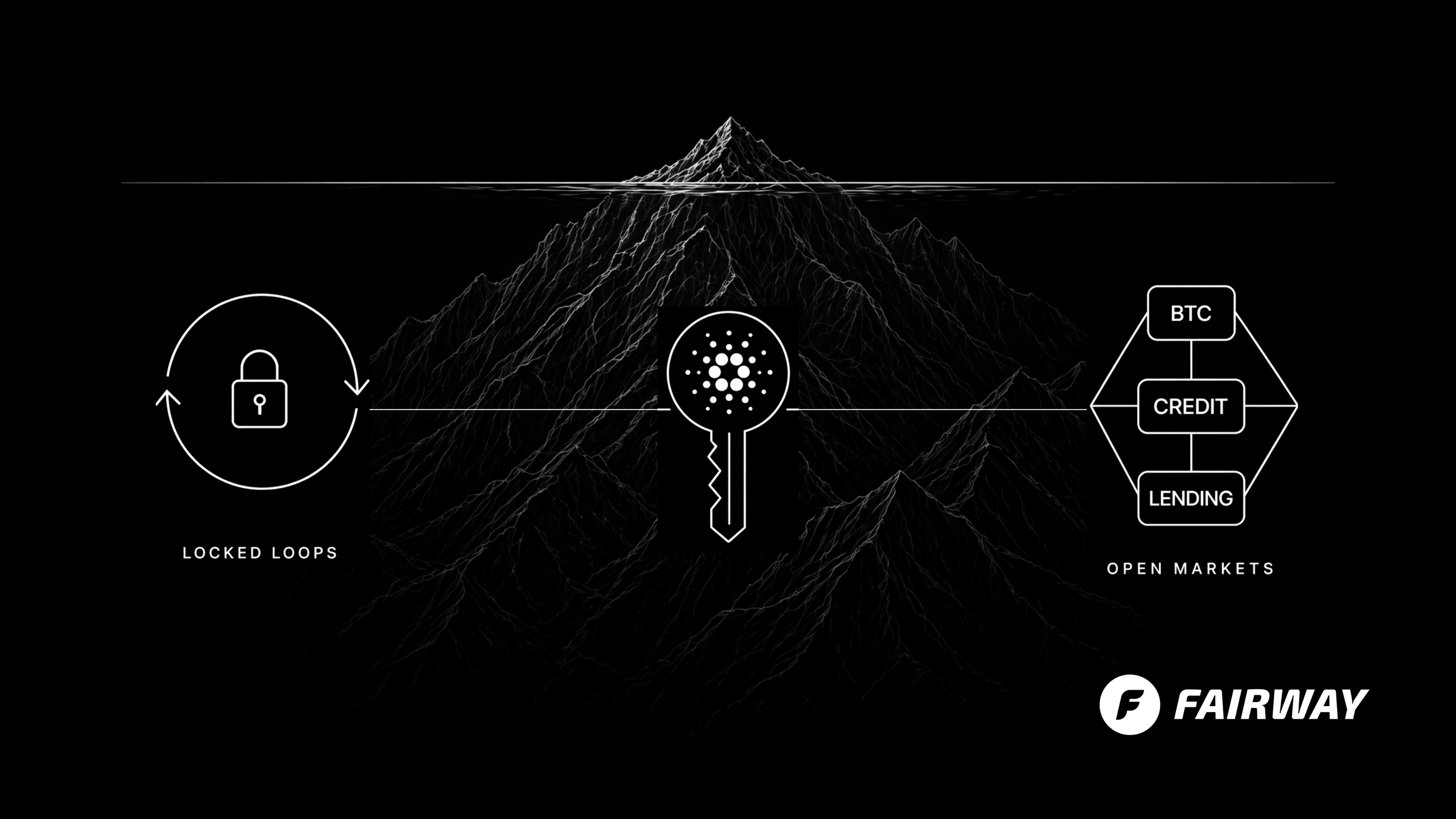

This is where Cardano may be quietly building something the wider crypto market has underestimated.

Cardano’s extended UTxO model is naturally suited to representing individual states and individual transactions onchain. Instead of treating everything as one mutable balance sheet, it can model separate financial objects: offers, claims, collateral positions, repayment states, rights, obligations, and transfers.

That may sound technical, but the commercial implication is straightforward.

Credit markets need granularity.

Borrowers vary. Loan durations vary. Collateral types vary. Jurisdictions vary. Underwriting criteria vary. Covenants vary. Risk tolerances vary.

Trying to force all of that into a single pooled model can be elegant in some contexts, but restrictive in others.

A marketplace built around specific intents and specific agreements can look much closer to how lending works in practice.

And more builders in the Cardano ecosystem appear to be recognizing that.

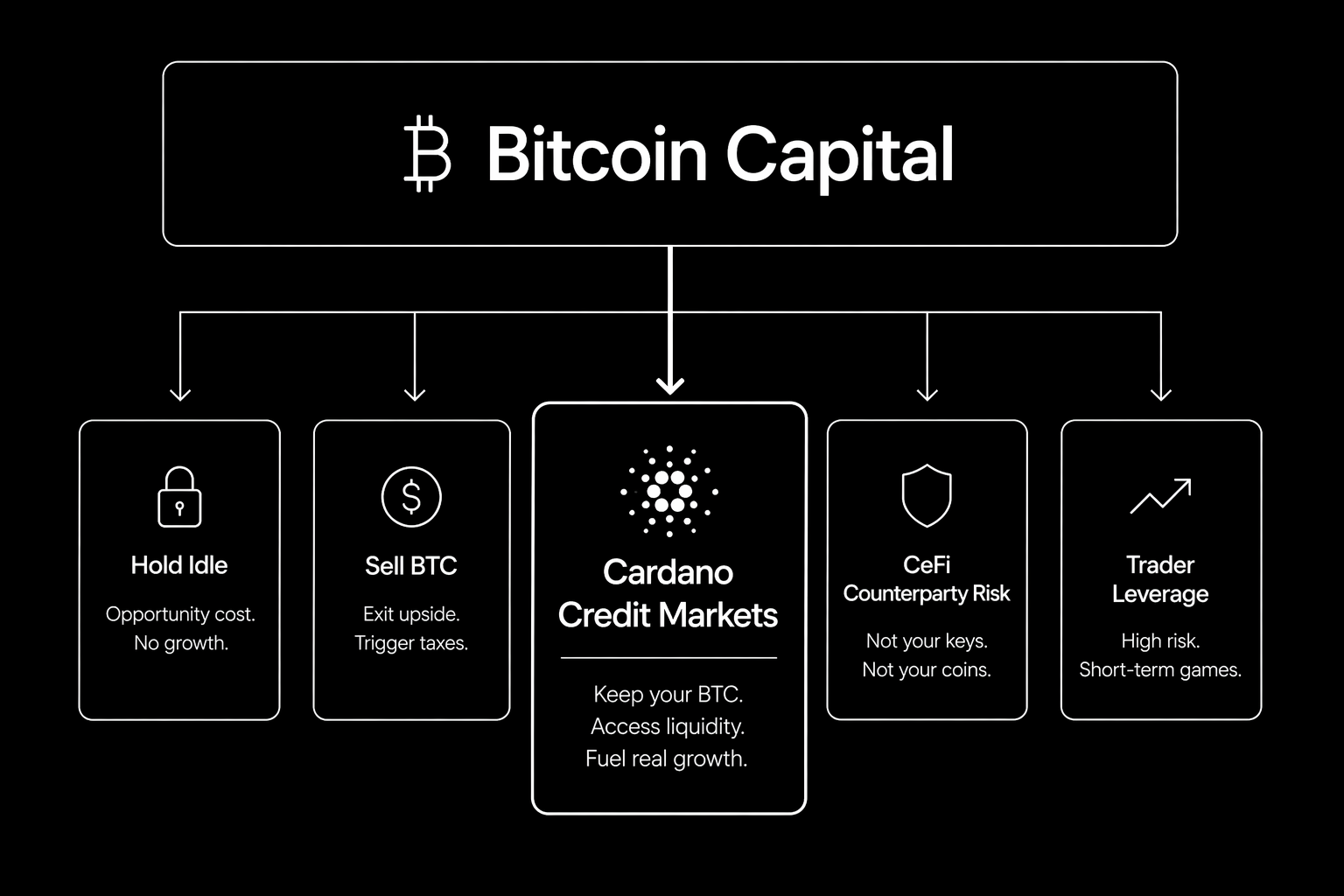

Bitcoin Could Be the First Major Use Case

There is also a capital source sitting in plain sight.

Bitcoin remains the largest pool of digital collateral in the world, yet much of it is economically idle.

BTC holders often face a narrow set of options:

- hold passively

- sell to raise liquidity

- trust centralized lenders

- enter leveraged systems designed for traders rather than lenders

That leaves an obvious gap in the market.

If Bitcoin can be used as collateral in transparent, peer-to-peer, non-margin credit markets, the result is not another speculative product. It is a practical financial service.

Capital gets deployed without forced selling. Borrowers gain access to liquidity. Lenders gain access to secured yield opportunities. Markets become more productive.

That is the kind of use case institutions understand immediately.

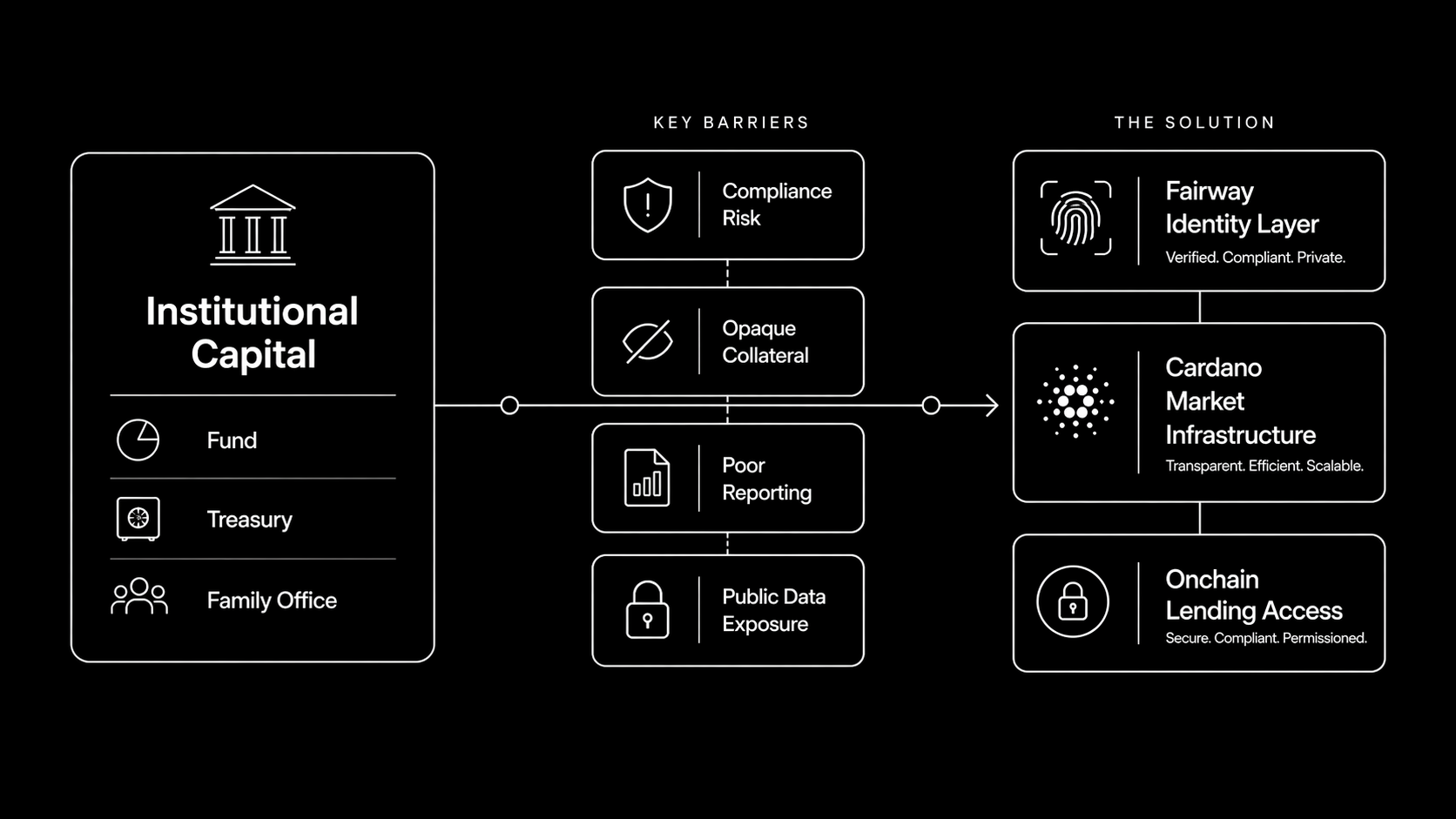

Institutions Don’t Need More Tokens

Traditional finance has spent years studying crypto. Selectively investing, selectively experimenting, mostly waiting.

They are not waiting for another governance token.

They are waiting for infrastructure that improves real workflows:

- collateral mobility

- compliant market access

- private credit issuance

- efficient settlement

- transparent reporting

- broader investor participation

If crypto wants larger pools of capital, it has to solve larger capital-market problems.

That means shifting from systems built around volatility extraction toward systems built around capital formation.

Cardano May Be Building What Crypto Promised

For years, crypto marketed itself as the future of finance while much of the industry concentrated on trading infrastructure.

Meanwhile, a quieter track has been developing:

- collateral-backed lending

- identity-aware participation layers

- programmable credit markets

- institution-ready settlement systems

- productive use of dormant digital assets

If those markets mature, they could matter far more than many of the narratives that dominated the last cycle.

And if they emerge on Cardano, some observers will describe it as unexpected.

It would be more accurate to call it overlooked.

The Next Trillion-Dollar Crypto Product May Not Be a Token

It may be a market.

A market that connects idle digital assets with real credit demand.

A market where Bitcoin becomes productive collateral rather than passive inventory.

A market where open blockchain rails can coexist with the requirements of serious capital.

“That outcome is still being built. Nothing is guaranteed.”

But if crypto eventually delivers genuine financial infrastructure at scale, it may look less like the products of the last cycle—and more like what Cardano is quietly working toward now.

Henrik Metsämäki

Expert in blockchain compliance and regulatory frameworks. Passionate about bridging traditional finance with decentralized technologies.