DeFi's Next Act II : From Fragmented Pools to a Shared Order Book

The rise of Hyperliquid and the return of the order book

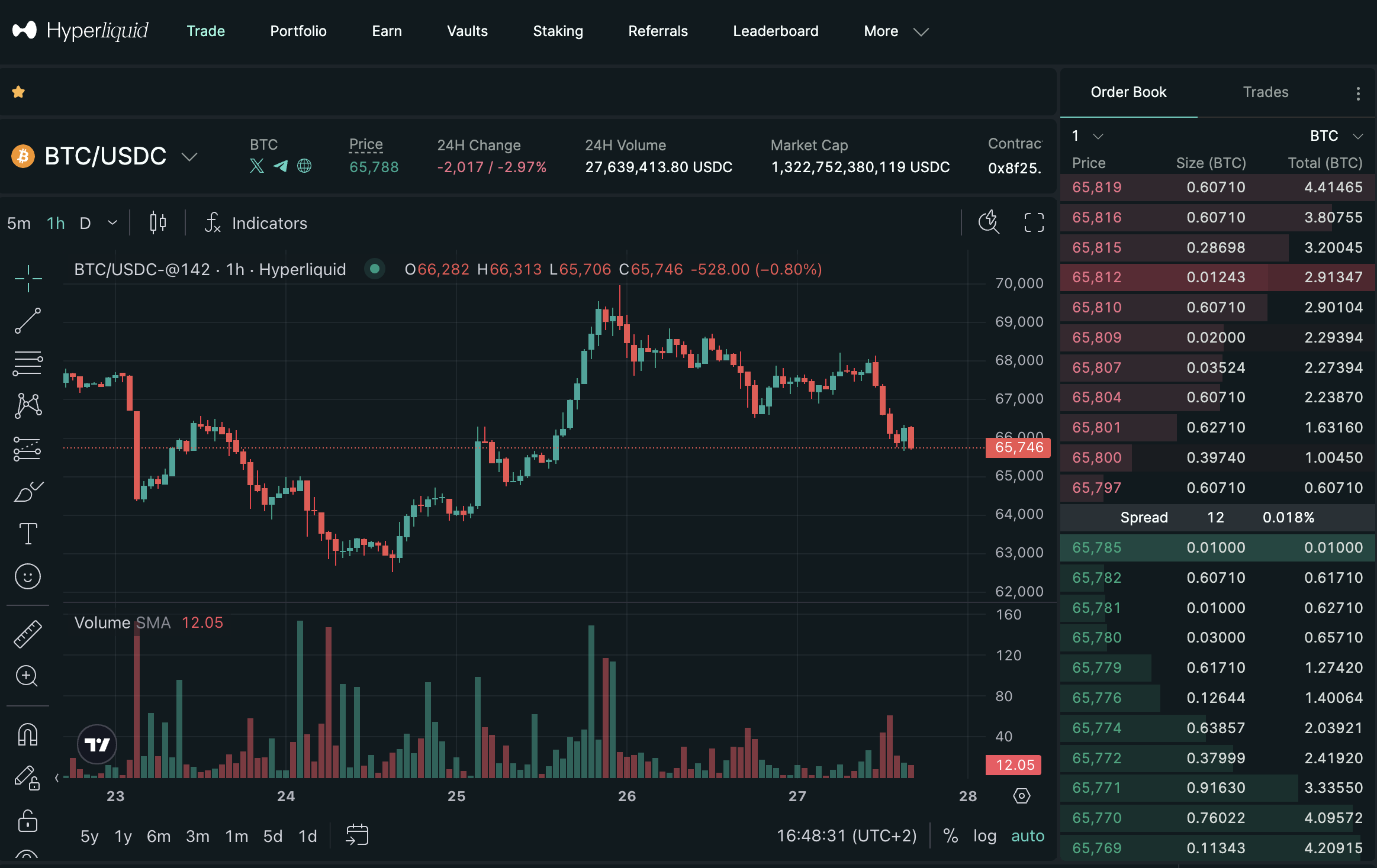

In late 2024 the DeFi narrative took a surprising turn. After years of automated market makers (AMMs) dominating on-chain trading, a new category of decentralised exchange began to gain traction: high-performance, central-limit-order-book (CLOB) platforms. The poster child is Hyperliquid, a protocol built on its own Layer 1 that replicates a centralised exchange experience without leaving the blockchain.

Hyperliquid's architecture is unusual for DeFi. Rather than a roll-up on Ethereum, it runs its own chain with a custom consensus (HyperBFT) and a Rust-based matching engine (HyperCore) tightly integrated into the base layer. This design lets every order and cancellation settle atomically on-chain with sub-millisecond execution and a throughput of over 200,000 transactions per second[1]. By unifying consensus, order matching and smart-contract execution under one validator set, Hyperliquid maintains a single shared state across perpetual futures, spot markets and DeFi contracts[2]. There are no bridges or cross-chain pools: liquidity is pooled globally within the system.

The results have been impressive. Hyperliquid's shared order-book model removed the fragmentation that plagues AMM-based perps and unified liquidity across products. Low latency (sub-0.1 s) and high throughput allow market-makers to maintain tight spreads, while its builder programme (HIP-3) allows third-party teams to deploy their own markets on the same infrastructure. By early 2026 it was processing hundreds of billions of dollars in monthly volume, capturing more than 30 % of on-chain perp trading and rivalling Binance on some pairs[3].

This success offers two lessons for the next generation of DeFi protocols:

- Shared liquidity matters. When traders and builders do not have to choose between a dozen shallow pools, depth increases and spreads tighten. Hyperliquid's unified state solves the “liquidity fragmentation” problem that plagues bridges and isolated roll-ups[1].

- Performance unlocks new participants. High throughput and deterministic matching attract market-makers, arbitrageurs and ultimately traditional traders who have been reluctant to touch DeFi.

But Hyperliquid's approach also comes with trade-offs. Running a dedicated chain is resource-intensive, and vertical integration centralises responsibility. It has experienced at least one major incident where a faulty risk-engine update forced developers to intervene. The protocol is currently maintained by a small core team; whether it can remain decentralised as it scales is still an open question.

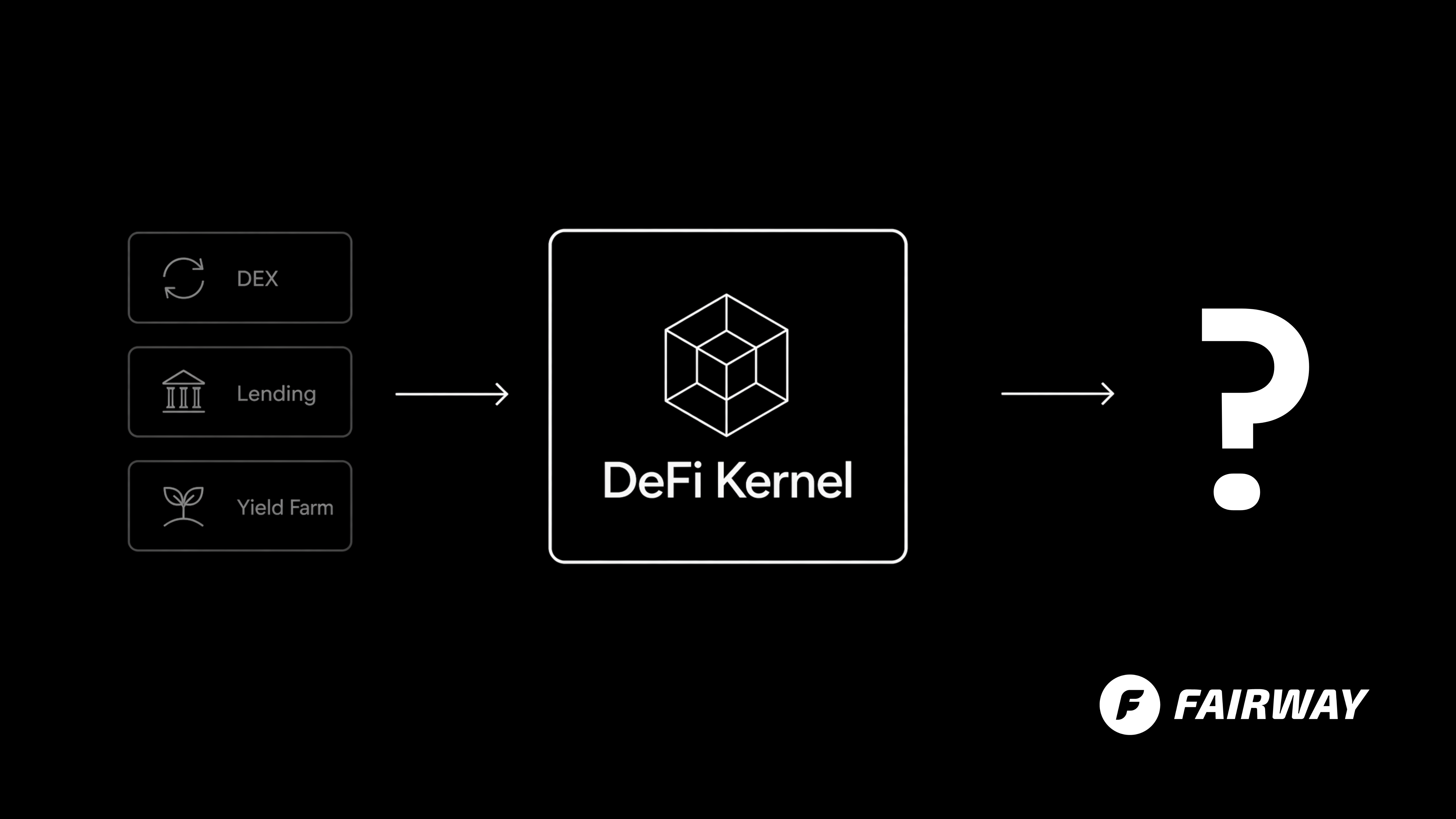

A Cardano-centric vision: protocol-level order books and layered services

While Hyperliquid shows what's possible when a DEX owns the entire stack, the Cardano ecosystem is coalescing around a different blueprint for on-chain finance. Rather than seeking a “Holy Grail” application that bundles matching engines, liquidity pools and user interfaces into one smart contract, several community developers – including Rusty (Fallen Icarus) – argue that Cardano should mirror traditional capital markets by separating roles into distinct layers.

In this vision, Cardano's Layer 1 acts as a bare-bones “kernel” that records loan requests and limit orders, while higher-throughput services handle matching, price enforcement, credit scoring and privacy.

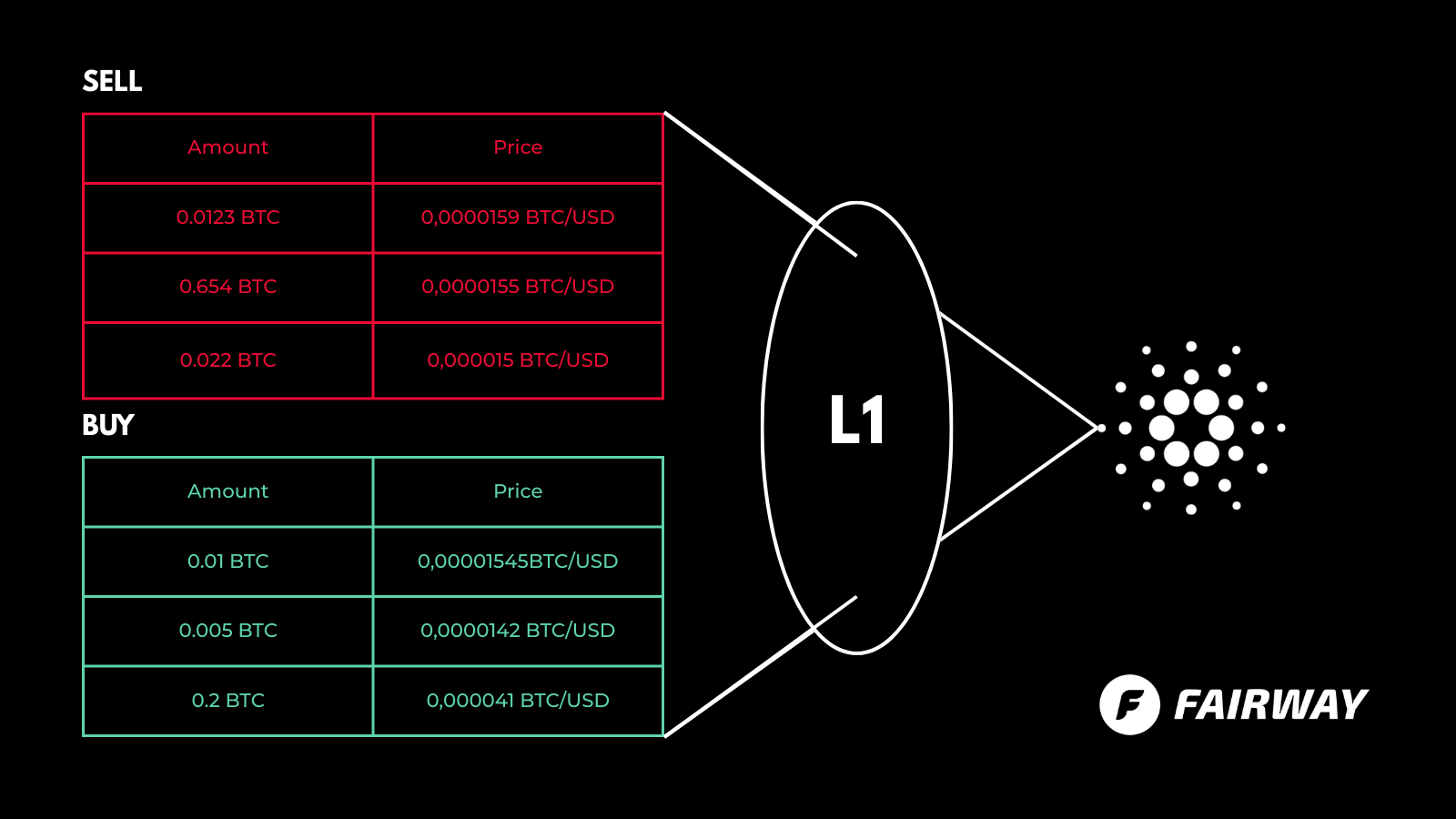

The inspiration comes from how the New York Stock Exchange operates. The exchange itself doesn't settle trades; that job falls to the DTCC, while brokers provide user interfaces. Translating this into the Cardano context means that the base ledger stores each order as a small UTxO tagged with a “beacon” token; anyone can scan the UTxO set to reconstruct the order book. Because the extended-UTxO model stores each message in its own cell rather than in a global mapping, the cost of posting an order doesn't increase as usage scales.

This layered approach offers several advantages:

- Anti-fragility. A simple base layer is easier to secure and audit. If a layer-2 matching engine fails, users can still post and settle orders directly on Layer 1.

- Permissionless innovation. Brokers, market makers and wallets can compete on top of the shared ledger without requiring permission from a central operator.

- Composability. By recording loan intents, swaps and options on the same ledger, users can bundle them atomically.

Identity and compliance are also core to this vision. Borrowers create credit avatars on-chain and attach zero-knowledge proofs of their KYC credentials in the transaction metadata. Off-chain indexers filter requests based on jurisdiction or risk policies, while the protocol itself remains open.

UTxO vs. account models: design matters

To appreciate why the Cardano community is doubling down on protocol-level order books, it helps to understand the trade-offs between UTxO-based chains and account-based chains like Ethereum.

Bookkeeping and parallelism

In a UTxO system every transaction consumes one or more unspent outputs and creates new outputs. There is no single “account balance”; instead, a wallet's balance is the sum of its UTxOs. Because outputs are independent, multiple transactions can be processed in parallel if they use disjoint UTxOs.

Determinism and predictability

Cardano's extended-UTxO model executes smart-contract code only when a specific UTxO is spent, and the validity of a transaction depends solely on its inputs.

Programmability and composability

The account model treats contracts like functions: they read and write a mutable global state. This is intuitive for developers and well-suited to pooling funds and automating liquidations.

Scalability and state growth

Because each UTxO is independent, verifying transactions in parallel is straightforward, and nodes can prune spent outputs.

Privacy and auditability

Wallets on UTxO chains often generate a new address for each transaction, making it harder to link a person's activities.

Suitability for P2P and non-margin lending

UTxO's locality makes it easy to treat each loan request or swap as an independent object whose storage cost does not grow with the number of participants.

In practice, both paradigms have their place. Ethereum's account model benefits from mature tooling, deep liquidity and network effects, which is why AMMs, stablecoins and lending pools found early success there. Cardano's UTxO model prioritises determinism, parallelism and privacy, making it attractive for building peer‑to‑peer credit markets and reputation‑based lending. At the same time, Cardano's privacy layer Midnight introduces an account‑based shielded ledger for private tokens and smart contracts. In other words, the Cardano stack natively offers both UTxO (public) and account‑style (private) components. A balanced approach might therefore combine elements of both: modelling each loan or order as a UTxO on the main chain while using Midnight's shielded accounts for pooled products or confidential smart contracts. This synergy between Cardano and Midnight provides a hybrid solution without needing to look to external ecosystems. Account abstraction and intent‑centric architectures are evolving on Ethereum, but they often rely on data‑availability networks and sequencers, introducing additional trust and censorship risks.

Can Cardano replicate Hyperliquid's success?

At first glance, Hyperliquid's rise may seem like proof that a unified orderbook and layered approach isn't needed. After all, Hyperliquid combines orderbook and matching in one L1 and still achieves massive adoption. But the two visions are not mutually exclusive:

- Hyperliquid demonstrates that users value unified liquidity and fast execution, and that a deep, shared order book can attract both retail traders and sophisticated market‑makers. Cardano's DeFi ecosystem currently suffers from fractured liquidity across AMM pools and isolated order books. The protocol‑level order book Rusty and others propose, addresses this by storing intents on the main chain and letting Layer‑2s compete to match them

- Hyperliquid's success also underscores the importance of builder‑friendly primitives. HIP‑3 allows external teams to launch their own perps markets on Hyperliquid's liquidity and earn a share of fees[4]. A Cardano order‑book kernel could provide similar hooks for wallets, arbitrage bots, derivatives markets and credit‑risk scoring services, without forcing them to rewrite the core logic.

- However, replicating Hyperliquid's performance on Cardano's Layer 1 is neither feasible nor desirable. Hyperliquid's custom chain achieves its throughput by tightly coupling matching and consensus[5]. Cardano's aim is different: robustness and neutrality, with throughput improvements delivered by projects like Midgard/Sundial (optimistic roll‑ups), Hydra (state channels) and Ouroboros Leios (L1 scaling). Midgard processes transactions off‑chain at high speed and periodically posts state roots back to Cardano, using the same extended‑UTxO model to maintain compatibility[6]. Sundial merges this scaling with a trust‑minimised Bitcoin bridge. A BitVM‑powered bridge locks BTC on the Bitcoin blockchain and issues a pegged BTC asset on Cardano; the wrapped BTC can then participate in Cardano DeFi and can be redeemed back to Bitcoin[7].

In this environment, a protocol‑level order book becomes a neutral liquidity layer accessible from both L1 and L2. Midgard or Hydra heads can batch and match orders at high speed and then publish the results back to the shared ledger. Sundial and various bridges bring Bitcoin liquidity and allow BTC‑denominated loans and swaps to settle on the same order book. Leios increases L1 throughput, making room for more intents and reducing confirmation times. Liquidity no longer fragments; it aggregates, because all paths lead back to a common UTxO set.

The road ahead: unlocking institutional capital and Bitcoin liquidity

DeFi is not a zero‑sum game. It evolves through iteration and synthesis. Hyperliquid shows that high‑performance on‑chain order books can beat centralised exchanges at their own game; this proposed approach shows how those order books can be turned into public goods that support borrowing, lending and identity without sacrificing decentralisation. Cardano's layered roadmap – from Ouroboros Leios at the base to Midgard and Hydra at Layer 2 and Midnight for privacy – is designed to accommodate this synthesis.

Bringing Bitcoin into the mix only increases the stakes. By locking BTC on the Bitcoin chain and issuing a trust‑minimised Bitcoin asset on Cardano[7], Sundial and various bridges aim to make hundreds of billions of dollars of dormant liquidity available to DeFi. Wrapped BTC could be posted as collateral in this proposed credit market, earn yield through non‑margin loans, or trade against ADA and USDM in a single, protocol‑level order book.

We are at the cusp of a new chapter for Cardano DeFi. The “Holy Grail” is not one application but a shared financial layer that anyone can build on. With a robust Layer 1, fast Layer‑2s, a common order book and a pathway for institutional capital and Bitcoin liquidity, the foundation is being laid for a flourishing ecosystem that honours decentralisation while embracing real‑world finance. Hyperliquid's success proves the appetite exists; the architecture that Rusty proposes in his videos shows how to capture it without compromising on principles. The story is just getting started.

Sources

[1][2] What is Hyperliquid and How Does it Work? (Explained)

https://www.quillaudits.com/blog/blockchain/what-is-hyperliquid

[3][4][5] HyperLiquid - The CLOB King - A1 Research

https://a1research.io/blog/hyperliquid-the-clob-king

[6] What's Next for Cardano in 2026

https://medium.com/tap-in-with-taptools/whats-next-for-cardano-in-2026-204c08949a1b

[7] Bitlayer BitVM and Sundial Set the Stage for Bitcoin on Cardano

https://medium.com/tap-in-with-taptools/bitlayer-bitvm-and-sundial-set-the-stage-for-bitcoin-on-cardano-3b1ae302305f

Henrik Metsämäki

Expert in blockchain compliance and regulatory frameworks. Passionate about bridging traditional finance with decentralized technologies.