DeFi’s Next Act I: Unlocking the Power of Non-Margin P2P Loans in DeFi

Decentralized finance (DeFi) has gained attention for its transparency, composability and open access. Yet most lending protocols today cater to traders, not builders. They offer margin loans—short-term credit that allows investors to leverage their positions. Margin debt across U.S. brokerages was about US$1.28 trillion [1], but U.S. household debt topped US$18.8 trillion [2]. That means margin loans represent only a tiny slice of the credit pie. Entrepreneurs or unbanked individuals seldom use them because a sudden price drop can liquidate their collateral and wipe out their capital.

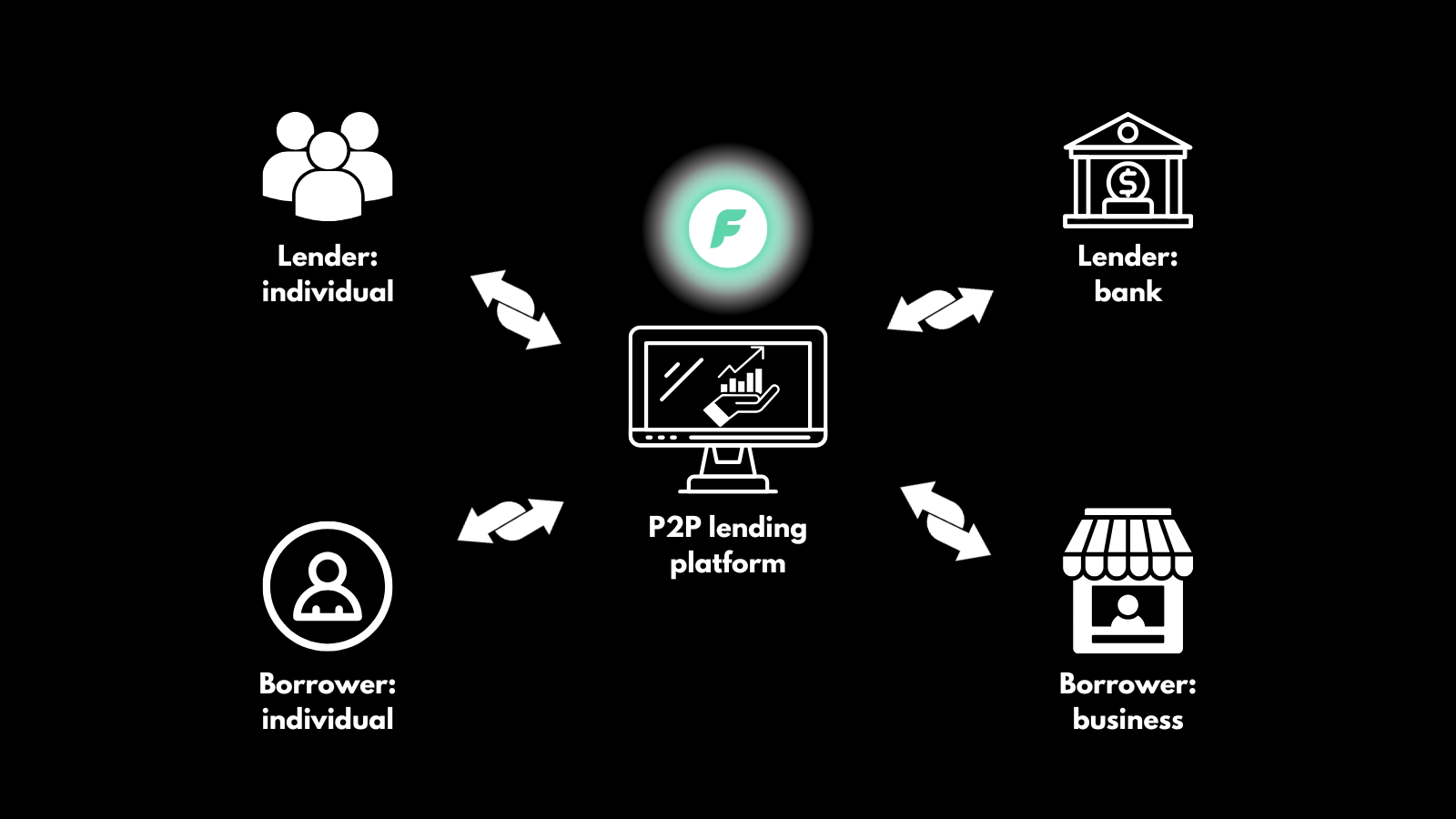

P2P lending is the real deal

In the wider economy, most loans are non-margin—you borrow to buy a home, start a business or pay for education, and you only lose collateral if you default, not because the market dipped. Traditional microfinance programs like Kiva demonstrate how powerful this can be: they’ve facilitated millions of loans with repayment rates around 96 % [3]. In East Africa, farmers who received microloans through the One Acre Fund saw their incomes rise by 40–50 % [4]. Clearly, small unsecured loans can ignite economic growth.

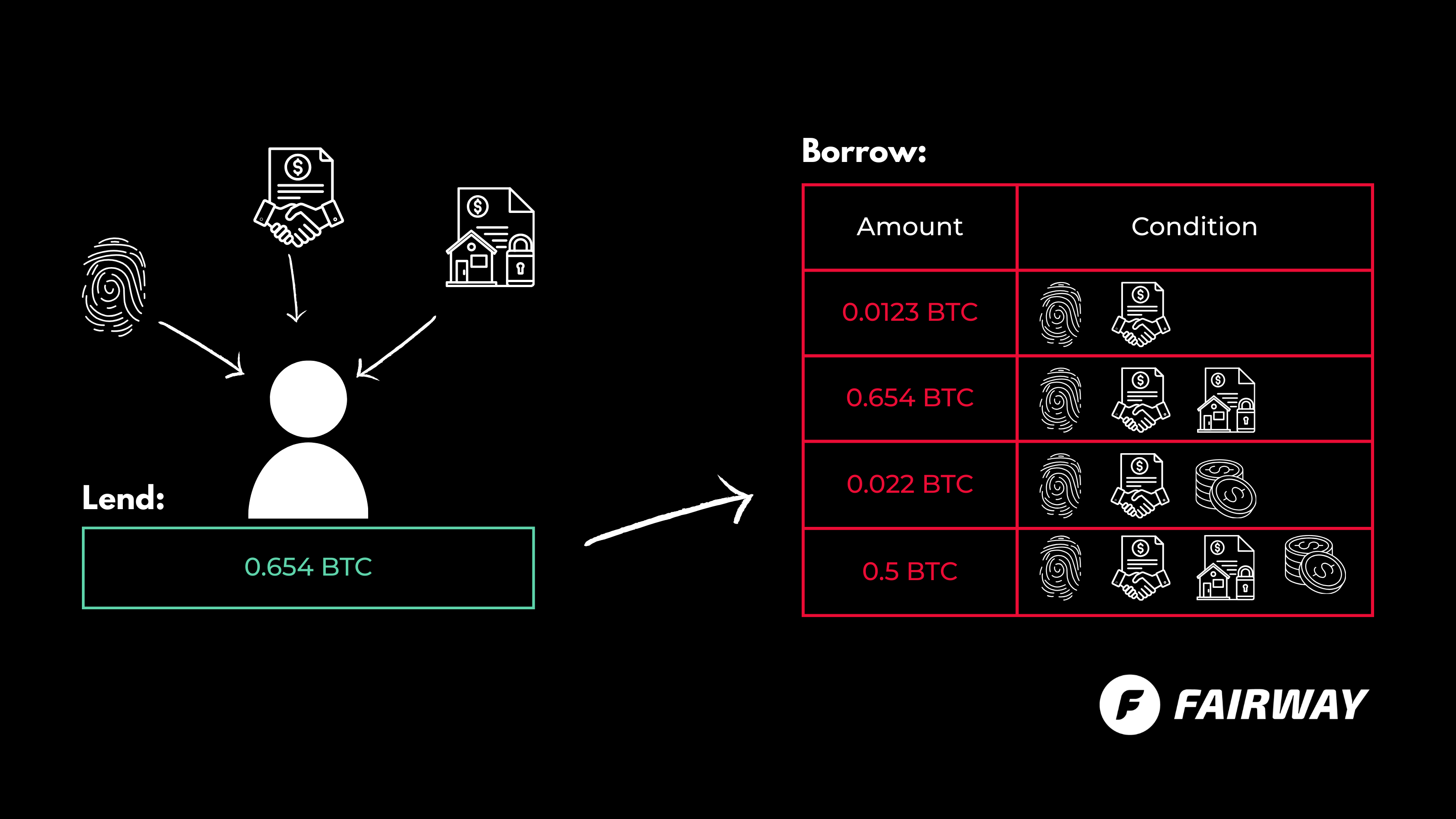

DeFi has an opportunity to replicate—and improve on—these models. Instead of pooling capital into an anonymous liquidity pool that automatically liquidates borrowers during volatility, peer-to-peer (P2P) non-margin loans let borrowers and lenders negotiate directly. Borrowers post a loan request on-chain with details like principal, term and (if they have it) collateral. Lenders respond with offers. When a loan is funded, the borrower keeps custody of their assets and only forfeits collateral if they fail to repay.

How it works under the hood

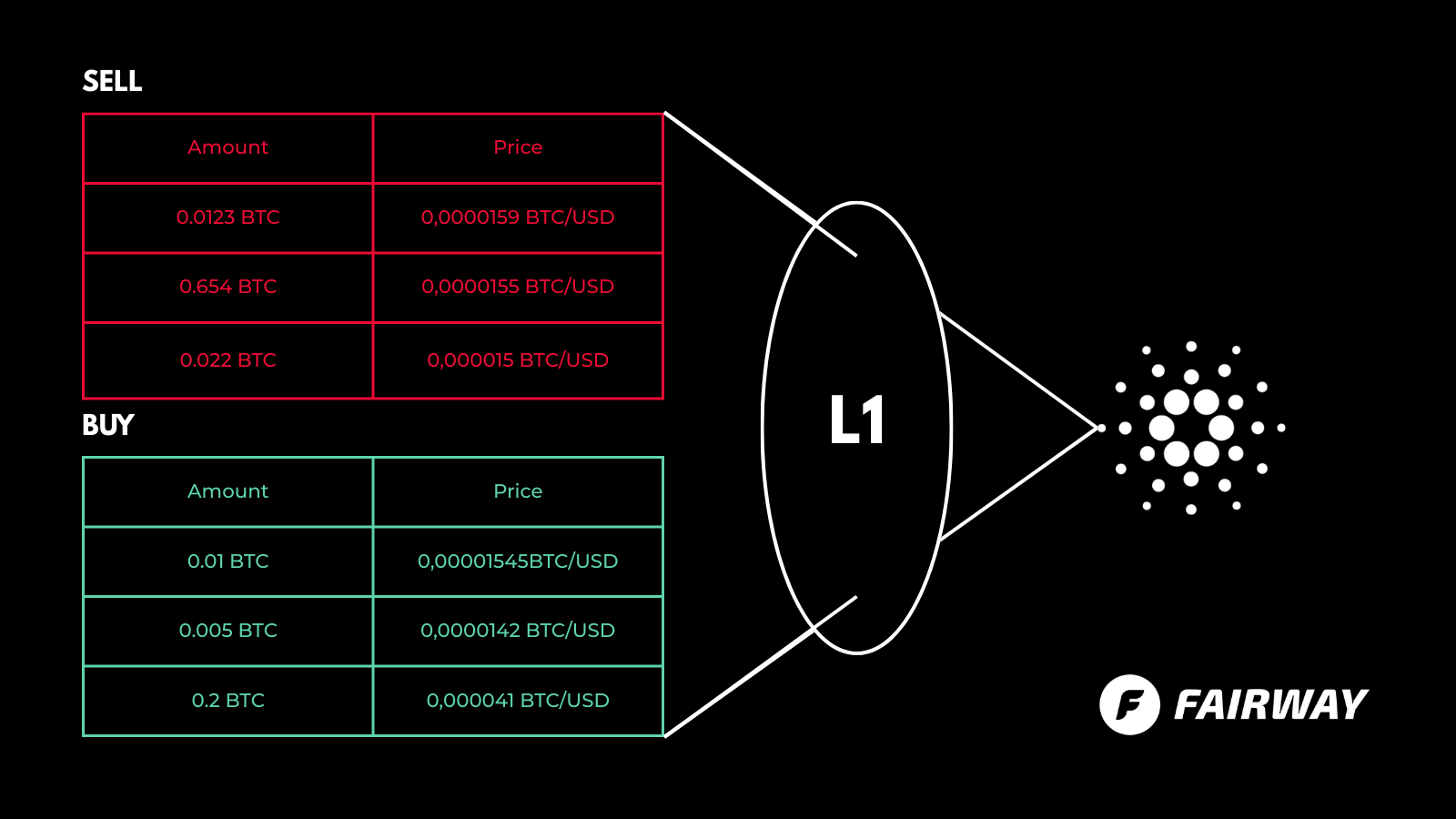

Cardano’s extended UTxO model makes P2P lending practical. Each loan request or offer lives in its own UTxO—essentially a tiny, unchangeable record on the blockchain. This design means anyone can independently see all active loan requests; there is no centralized database to trust. It also scales efficiently. Proposals like CIP-89 suggest using beacon tokens to tag loan transactions so off-chain indexers can quickly filter and display them [5].

Because the loan’s lifecycle—offer, acceptance, repayment or default—is recorded publicly, borrowers build a credit history visible to all. Good borrowers gain reputational capital they can leverage for larger or even under-collateralized loans. This mirrors how credit scores work today but without relying on opaque credit bureaus.

Identity and privacy

One of the hardest problems in peer-to-peer lending is trust: how do you know the borrower isn’t a scammer? Traditional lenders solve this with Know-Your-Customer (KYC) checks that verify a person’s name, date of birth, address and national ID number [6]. Regulators such as the U.S. Treasury’s Bank Secrecy Act require financial institutions to identify and verify customers and beneficial owners and to monitor transactions [7]. Any DeFi protocol that wants access to serious capital—including capital from regulated institutions—must therefore integrate identity in a way that meets these requirements without compromising user privacy.

Fairway is currently building that identity layer. Our work focuses on leveraging Midnight and modern cryptography to issue verifiable KYC credentials that stay off-chain. Borrowers will be able to attach zero-knowledge proofs of those credentials to their loan requests, proving they are verified without revealing their personal data. Off-chain indexers and wallet interfaces will then be able to filter loan requests to show only those from verified participants.

This mirrors the credit-avatar concept explored by some Cardano developers such as Fallen Icarus [8]: a borrower maintains a public address that accumulates on-chain reputation, while their personal data and funds live on Midnight.

Fairway’s architecture also supports private intents so users can submit encrypted loan intents or trading orders through Midnight and have them routed to the public order book only when execution is possible. This preserves confidentiality around strategy while keeping market data public and auditable.

Once ready, these capabilities could be applied beyond Cardano: Bitcoin holders using bridged BTC or other assets could leverage Fairway credentials and private intents to participate in non-margin lending within a regulatory-friendly framework.

In short, Fairway enables the identity layer needed for mainstream adoption of P2P lending. By combining zero-knowledge credentials, privacy-preserving intents and a public credit history, Fairway’s stack lets DeFi serve both retail borrowers and regulated institutions—on Cardano today and on Bitcoin DeFi tomorrow.

Bridging crypto and traditional finance

Once you can originate millions of small, verifiable loans on-chain, you can combine them into loan-backed securities, much like mortgage-backed securities in traditional markets. Packaging loans diversifies risk: if one borrower defaults, the others in the pool continue to pay, reducing losses [9]. These packaged assets can be sold to investors who might not want to manually assess individual borrowers but are comfortable buying a diversified slice of many loans. That’s how P2P lending becomes a bridge between crypto capital and mainstream finance.

Beyond speculation

Non-margin P2P lending turns DeFi into a tool for real economic activity. Instead of just enabling leveraged bets on tokens, it provides credit to entrepreneurs and under-banked communities. It preserves privacy and censorship resistance while meeting regulatory obligations through verifiable credentials. And by recording every loan on a public ledger, it creates an open, auditable credit market that doesn’t rely on intermediaries.

Sources

- Advisor Perspectives: U.S. margin debt was about $1.28 trillion in January 2026 Click Here.

- Reuters: U.S. household debt reached $18.8 trillion in Q4 2025 Click Here.

- Kiva due diligence: overall repayment rate ~96.3% Click Here.

- CGAA article: One Acre Fund microloans increased farmers’ incomes by 40–50% Click Here.

- CIP-89 and beacon tokens for on-chain credit history (Fallen Icarus) Click Here.

- KYC requirements overview Click Here.

- FinCEN Customer Due Diligence rule Click Here.

- Privacy front-end concept (Fallen Icarus) Click Here.

- Packaging microloans reduces default risk in loan-backed securities (Fallen Icarus) Click Here.

Henrik Metsämäki

Expert in blockchain compliance and regulatory frameworks. Passionate about bridging traditional finance with decentralized technologies.